.svg)

BaaS, embedded finance, and open banking; they don’t mean the same thing

There’s a lot of jargon floating around in fintech. You’ve probably heard terms like Banking-as-a-Service, embedded finance, and open banking often used interchangeably.

But they don’t mean the same thing.

Meet three builders: Lisa, Amir, and Priya.

They’re all building fintech products, but each takes a very different approach, and for good reason.

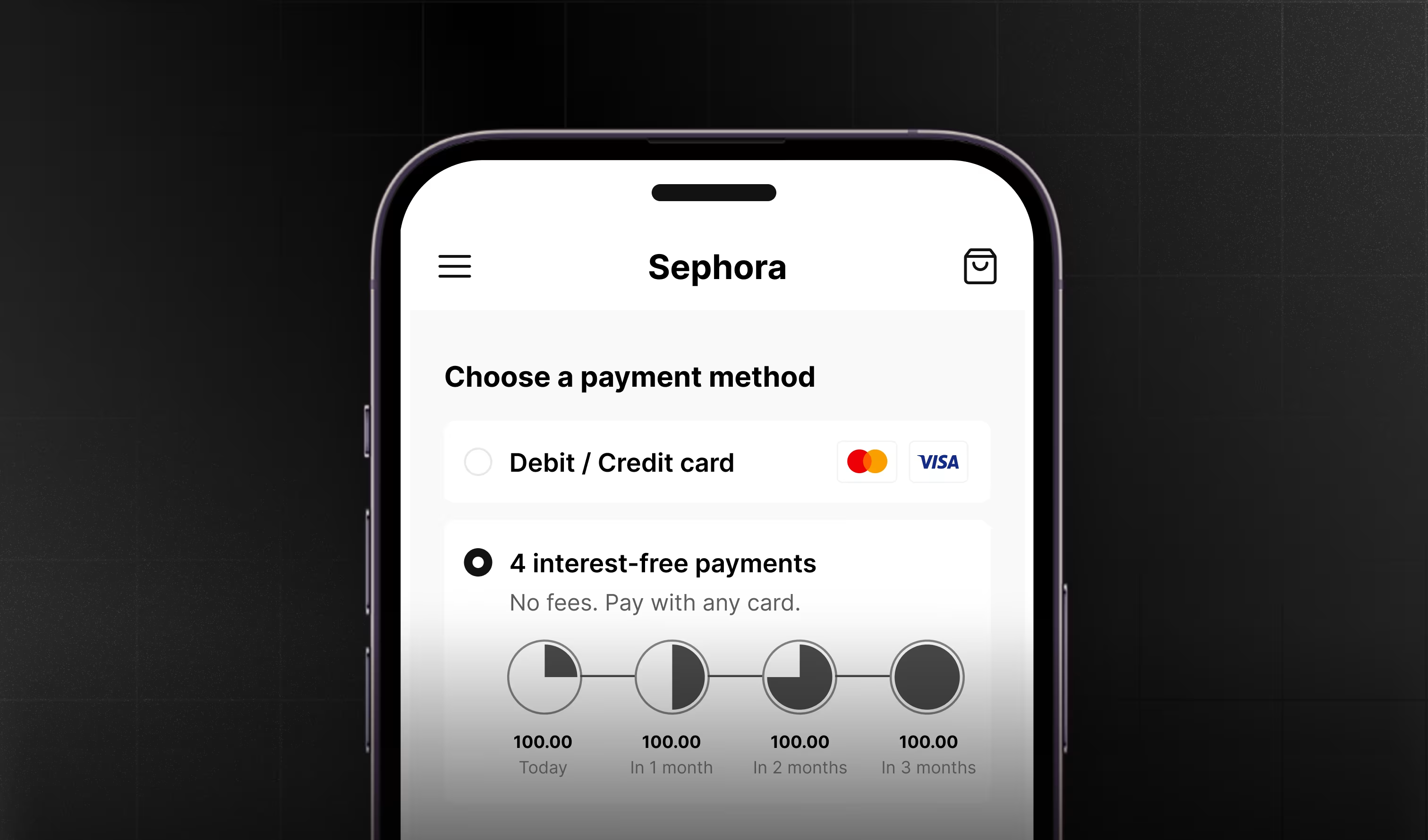

Lisa is launching a challenger bank.

She wants to offer customers the ability to sign up, open an account, get a debit card, send and receive money, and even access credit.

But Lisa doesn’t have a banking license and doesn’t want to spend 3+ years getting one.

So she turns to Banking-as-a-Service (BaaS).

BaaS providers sit between licensed banks and fintech builders, offering APIs that allow companies like Lisa’s to build regulated products without becoming a bank themselves.

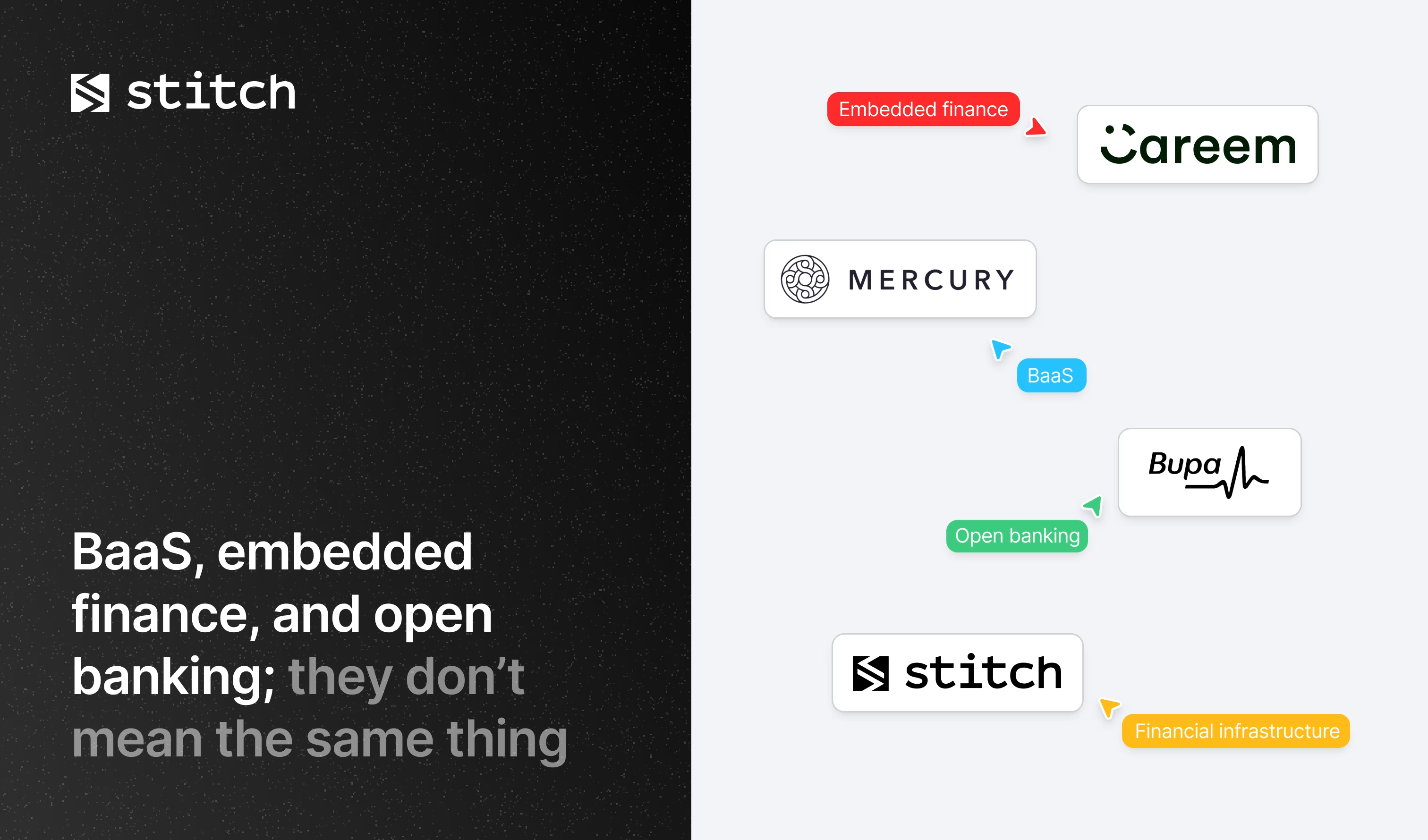

Embedded finance is not relevant here because she’s not embedding services into another product because this is the product. And neither is open banking because she’s not connecting to other banks, she’s offering her own accounts. Think Mercury, Wio, or Monzo. These challenger banks built on top of BaaS providers to bring products to market without holding a banking license.

Amir runs a ride-hailing platform.

He doesn’t want to become a bank. But he wants his drivers to get paid instantly after each ride, access fuel discounts, and take out short-term loans, without leaving his app.

So he uses embedded finance.

Here, the financial features are not the product. They’re baked into an existing user journey. Drivers aren’t opening an account with a new bank, they’re simply unlocking more value from a platform they already use. BaaS is not relevant here because Amir isn’t building a financial institution. He’s embedding finance into a non-financial experience. Neither is open banking because no bank connections are being made.

Think Careem or Uber offering drivers instant pay or Shopify Capital giving merchants small business loans within the dashboard.

Priya is building a personal finance app.

She wants her users to connect all their bank accounts, track their spending, and get savings insights. So she uses Open Banking APIs to fetch real-time data from users’ existing accounts, with their consent. Embedded finance is not relevant here because this is a financial product, not a non-financial one. Neither is BaaS because she’s not issuing accounts, cards, or loans.

Think Bupa, Sarwa, or Mint, apps that aggregate account info through APIs.

To simplify further, one wants to be a bank (BaaS), one simply wants to offer financial/banking features inside a non financial product (embedded finance), and one wants to connect to banks (open banking).

So where does financial infrastructure come in?

It’s the foundation of it all.

- Lisa needs reliable ledgers, account creation, and compliance flows.

- Amir needs payouts, underwriting, and fraud detection.

- Priya needs secure data processing and reporting tools.

None of them want to reinvent the wheel. And that’s where modern financial infrastructure platforms come in, offering the technical foundation behind money movement, compliance, and product operations.

Think Stitch, the unified platform offering ledgers, lending systems, card issuing, deposits, and more. Builders plug in what they need and go to market fast.

There’s no one-size-fits-all approach to fintech. The right model depends on what you’re building.

But if there’s one thing all builders need, from fintechs to banks to platforms, it’s solid infrastructure.

Modern players like Stitch bring all the essential tools together: real-time ledgering, lending engines, deposit infrastructure, onboarding, compliance, payments. Modular, API-first, and built for regulated environments.

Whether you’re building a bank, embedding payments, or just trying to reduce operational drag, you don’t need more vendors. You need better infrastructure