.svg)

The rise of Buy Now, Pay Later and what it takes to make it work

It usually starts with a simple choice.

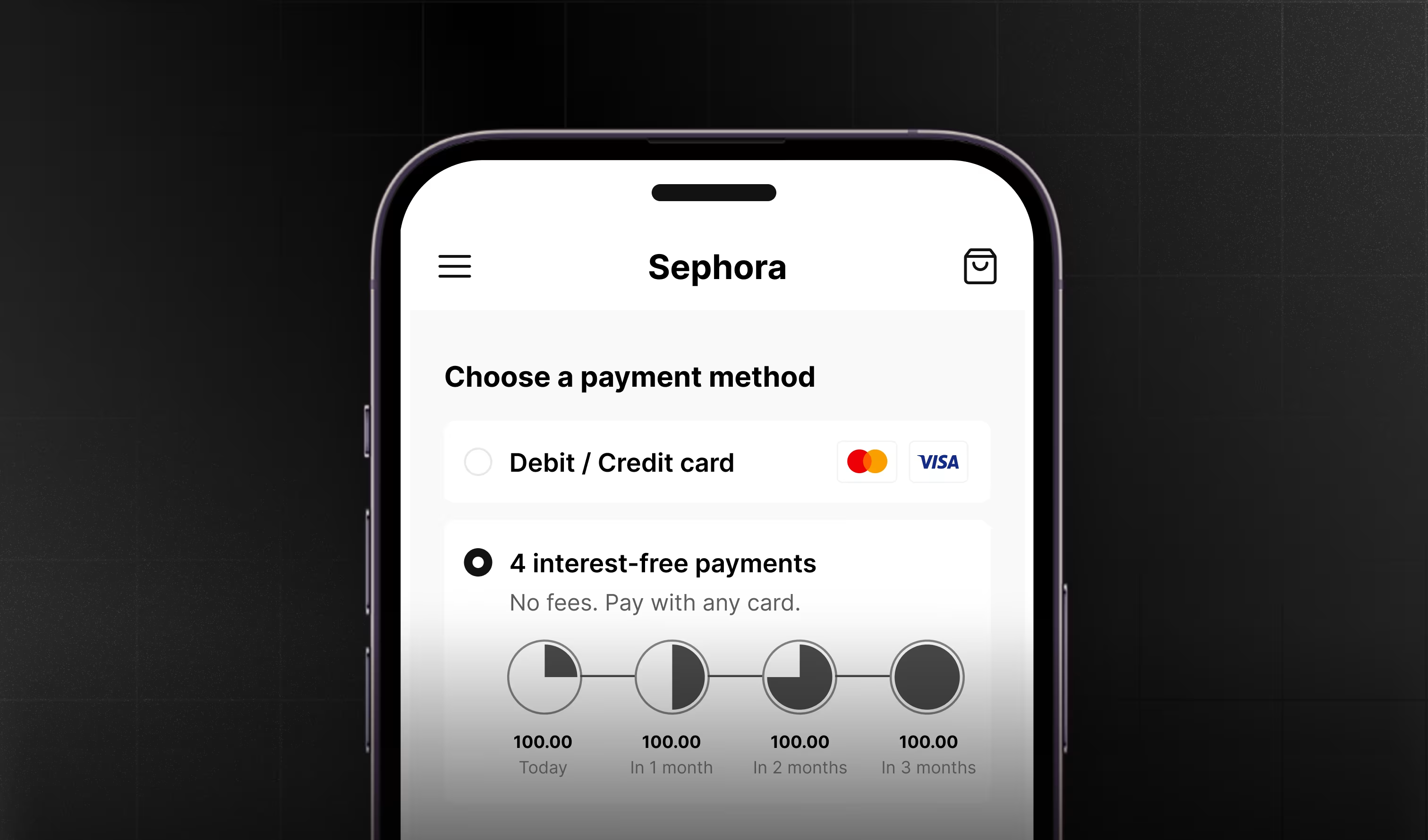

At checkout, next to card and bank transfer, a new option appears. Pay in four. No interest. No paperwork. No friction.

Buy Now, Pay Later, or BNPL, has quietly reshaped how people pay, how merchants sell, and how credit flows across the world.

From deferred payments to embedded credit

Deferred payment is not new. Installments have existed for decades, from department store credit to layaway programs and consumer financing at the point of sale.

What changed was speed.

BNPL compressed credit approval, risk assessment, payment execution, and settlement into a few seconds. No branch visits. No long forms. No waiting period.

A customer taps once, a credit decision is made in the background, and a purchase is completed instantly.

That shift turned credit into something that feels less like a financial product and more like a feature of checkout.

And once credit becomes embedded, it scales fast.

Why BNPL went global so quickly

BNPL gained traction because it solved problems on both sides of the transaction, and the numbers tell the story of just how quickly that happened.

For consumers, it offered flexible financing without traditional credit card baggage. For merchants, it unlocked higher conversion rates and larger cart sizes. Together, these forces helped BNPL move from a fringe offering to a core payment method in just a few years.

Globally, the scale of this shift is remarkable. The total BNPL market is projected to grow more than 13 percent year over year as millions of consumers opt for flexible payments at checkout.

User adoption paints an even more striking picture. Worldwide BNPL users numbered roughly 360 million as of 2024, with forecasts suggesting this could nearly double to 900 million by 2027.

That level of adoption reshaped the pay-later landscape and made BNPL a fixture at many payment touch-points internationally.

At the heart of all this growth was a simple premise: offer credit that feels like part of the checkout experience rather than a separate, intimidating financial product. And while the experience stayed simple on the surface, the infrastructure beneath had to scale, adapt, and integrate with existing payment systems everywhere it landed.

What really happens when a BNPL transaction is approved

Behind that one-click approval is a chain of coordinated systems working in real time.

A typical BNPL flow involves:

- Identity and eligibility checks

- Risk and affordability assessment

- Credit decisioning

- Payment authorization

- Disbursement to the merchant

- Scheduled collections from the customer

- Ongoing reconciliation, retries, and reporting

None of this is visible to the customer. It is designed not to be.

But as BNPL volumes grow, this invisible layer becomes more complex, more regulated, and more critical to get right; at scale, an orchestration problem.

The infrastructure challenge beneath BNPL

As BNPL providers expand across regions and use cases, they face a common set of challenges:

- Multiple payment methods and local rails

- Real-time decisioning requirements

- High-frequency collections and retries

- Regulatory oversight across jurisdictions

- Tight reconciliation between lenders, merchants, and banks

Many early BNPL players built vertically integrated stacks to move fast. That worked initially.

But growth introduces friction.

New markets require new integrations. New products demand more configurable logic. New regulations increase operational overhead.

BNPL, at its core, relies on infrastructure that can connect payments, credit logic, and lifecycle management without becoming brittle.

BNPL as a system, not a product

The most resilient BNPL models treat installment payments as a system rather than a standalone product.

That system needs to:

- Route payments intelligently

- Apply rules dynamically

- Handle failures gracefully

- Adapt to different risk profiles and repayment models

This is where BNPL infrastructure platforms quietly step in.

Instead of rebuilding the same logic repeatedly, modern BNPL stacks increasingly rely on modular components that can be configured, extended, and scaled.

Credit is no longer hard-coded. It is orchestrated.

Where infrastructure platforms fit in

Infrastructure platforms like Stitch sit beneath the BNPL experience, not in front of it.

They provide the connective tissue between:

- Payment rails

- Decisioning engines

- Loan or installment management

- Reconciliation and reporting systems

By abstracting complexity, infrastructure allows BNPL providers, banks, and fintechs to focus on product design, risk models, and customer experience.

The result is faster iteration without sacrificing control.

In the same way a unified switch coordinates payments, BNPL infrastructure coordinates credit events across the lifecycle of a transaction.

The next phase of BNPL

BNPL is evolving.

We are already seeing:

- Longer-term installment products

- BNPL embedded into wallets and super apps

- Banks re-entering the space with regulated offerings

- Merchants building proprietary installment options

As BNPL matures, success will depend less on flashy checkout buttons and more on robust, adaptable infrastructure underneath.

Because when credit becomes embedded everywhere, the systems that manage it must be invisible, flexible, and dependable.