.svg)

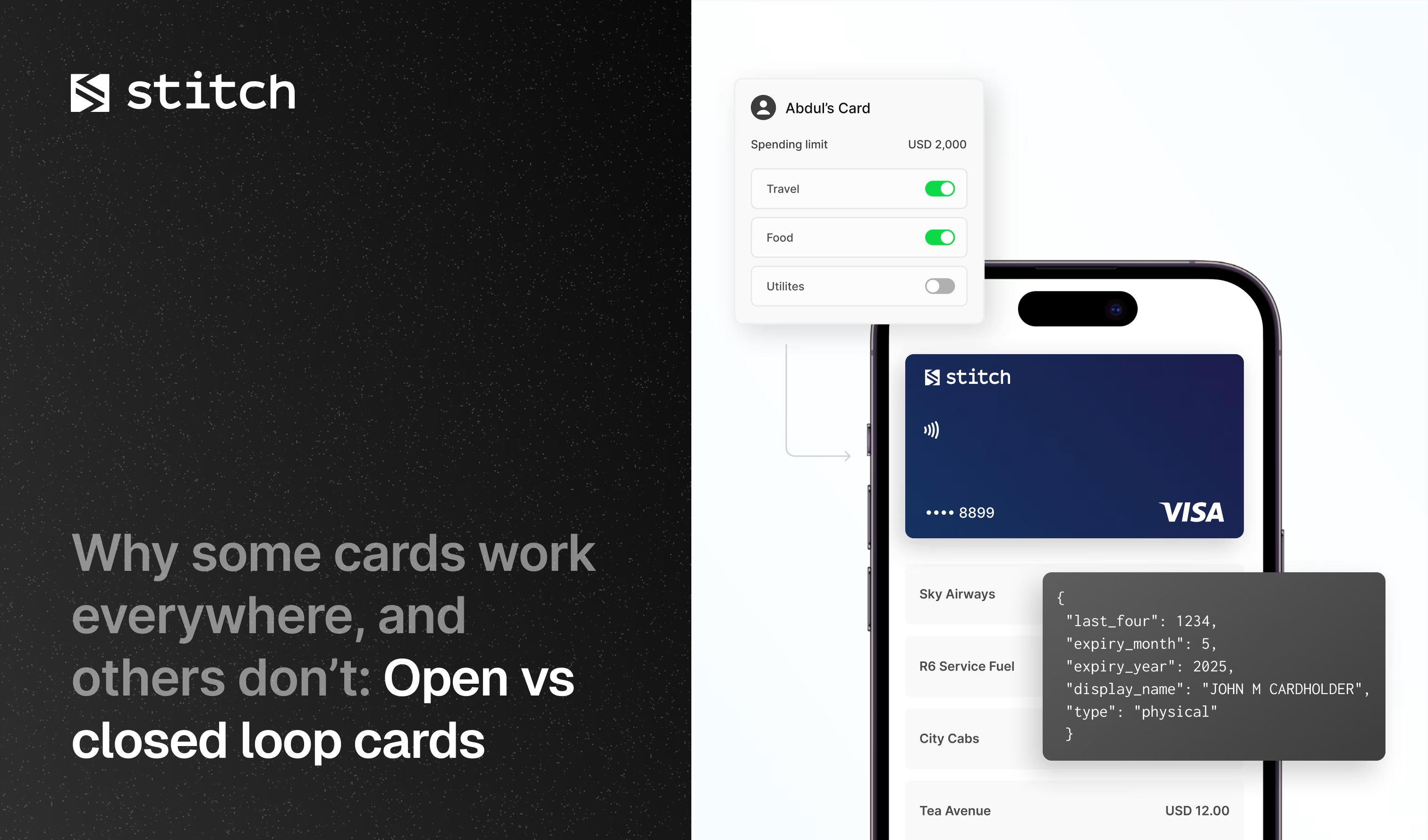

Why some cards work everywhere, and others don’t: Open vs closed loop cards

Danielle reached for her wallet at her favorite café in Milan. She wanted a quick coffee before her next meeting. She had two cards in her hand: one from her bank, usable anywhere in the world, and another from the café itself, only accepted in its stores. She paused. Unknowingly, Maya was holding two very different worlds of payments in her hands.

Every time a card swipes, taps, or clicks online, a hidden decision determines how that payment flows. Some cards give you freedom everywhere. Others tether you to a single ecosystem. These are the open loop and closed loop cards.

At first glance, all cards might look alike: a rectangle of plastic or a number on a screen. But when taking a closer look, how they move money, collect data, and unlock opportunities is entirely different. Understanding the distinction can be the difference between flexibility and control, reach and loyalty, efficiency and cost.

Open loop cards

Open loop cards are the cards you know well. They are the ones backed by global payment networks like Visa, Mastercard, or American Express. Swipe it at a coffee shop or use it online, and it works seamlessly. Open loop cards rely on networks that span millions of merchants. Banks, payment processors, and networks work together to ensure every transaction is authorized, secure, and settled.

- Universal acceptance: Use them almost anywhere.

- Rewards and incentives: Cash-backs, points, and perks often follow the card.

- Consumer trust: These networks are built on decades of secure and reliable transactions.

But freedom comes at a cost. Transaction fees are higher, and customer data is dispersed across multiple entities, limiting the insights a single company can gather.

Closed loop cards

Closed loop cards, by contrast, are tightly woven into a single company’s ecosystem. Think of store gift cards, transit passes, or proprietary loyalty cards. These cards work only where the issuing company controls the system.

- Lower costs: Fewer intermediaries mean cheaper transactions.

- Direct customer insights: Every swipe tells the company exactly what their customer wants.

- Brand loyalty: Closed loop cards create habits and make leaving the ecosystem inconvenient.

For consumers, the trade-off is less freedom. They can only use the card where it’s accepted. But for businesses, this controlled environment unlocks personalized experiences, targeted rewards, and deeper relationships.

When each makes sense

- Open loop: Perfect for banks, fintechs, and platforms aiming for broad reach, seamless integration, and instant trust.

- Closed loop: Ideal for retailers, transit authorities, and service providers who want to deepen loyalty, reduce costs, and collect actionable customer insights.

Many companies today are exploring hybrid approaches, combining open loop reach with closed loop control, creating a payment ecosystem that is both flexible and insightful.

The future of cards

As Danielle decided which card to use, she didn’t see the invisible forces at work. She only experienced the outcome: instant approval, a seamless purchase, and the quiet efficiency that made it all feel effortless. But behind the scenes, two very different philosophies were shaping her payment journey; the open loop network, built for scale and freedom, and the closed loop system, designed for control and connection.

The payment landscape is evolving faster than ever. Real-time authorization, tokenization, and embedded finance are rewriting the rules. Open loop cards will continue to offer freedom at scale. Closed loop cards will deepen engagement in targeted ecosystems. And as technology advances, the line between the two may blur, giving both consumers and businesses the best of both worlds.